Environmental and Social Compensation Metrics: Walking the Talk?

April 25, 2019

Environmental and Social (E&S) compensation metrics are being brought into the spotlight as E&S issues are top of mind with stakeholders. Investors, employees and the general public want to understand how organizations are addressing climate change, human rights and pay equity among other topics that hit the headlines every day. As corporate governance has become an important aspect of oversight, issuers have been challenged by organizations such as Principles of Responsible Investment (PRI) to incorporate E&S into their executive compensation metrics.

In executive compensation consulting, it’s important that the board, management and compensation consultant work closely together to select incentives thoughtfully, because at the end of the year these will be the compensation metrics to which the executive team will be held. In the last three Farient Briefs, we have looked at E&S issues: the number of proxy proposals in the US, how large investors have supported those proposals, and the global trends in E&S proxy proposals. In the final installment of this series, we examine E&S incentives. With all the talk of E&S issues, are compensation committees tying executives’ pay to improving the E&S profile of their organizations or just giving it lip service?

Farient Brief Findings: What Surprised us at a Glance

- Environmental and Social (E&S) metrics are almost exclusively used in STI plans

- E&S metrics are typically tied to less than 10 percent of the overall STI award

- E&S goals aren’t well defined or disclosed, which often translates to a large discretionary component

E&S Compensation Metrics in Pay Plans

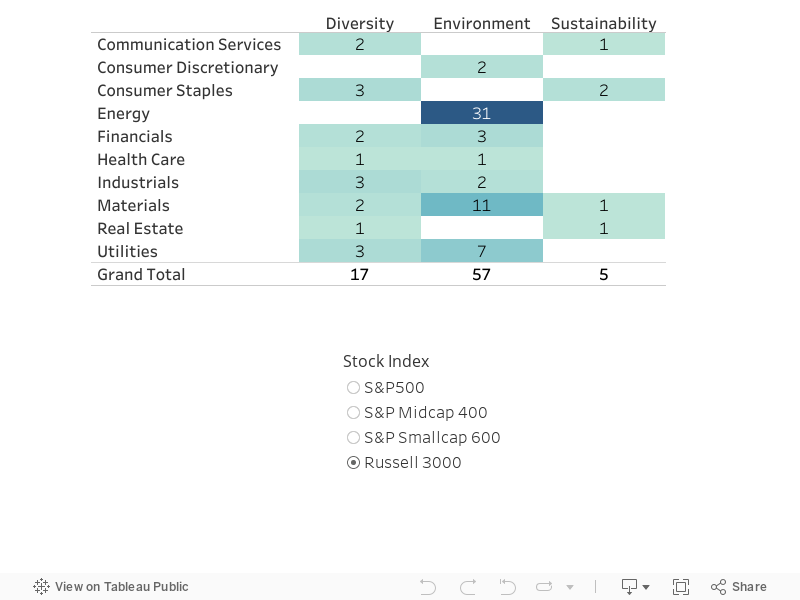

The Farient team examined compensation plans from companies in the Russell 3000 and found that E&S compensation metrics are almost exclusively used in determining annual bonuses. As would be expected, we found a concentration of companies – 57 specifically – in the energy, materials (think mining) and utilities sectors that were using environmental compensation metrics in these plans. Twenty five of these companies were in the S&P 500. But other metrics in the E&S category were few with only 18 companies using metrics around “diversity” and nine using “sustainability.

“There’s an old saying that what doesn’t get measured doesn’t get done. Nothing gets executive attention more effectively than linking E&S metrics to pay.” To that end, some companies may be taking a “wait and see” attitude to understand exactly what environmental and social regulations may be implemented, especially as we approach a presidential election in 2020. Still, many companies will be impacted by shareholders and other stakeholders and will want to incorporate best practices, like we have seen with Royal Dutch Shell, Chevron and Verizon, mentioned in this Brief, in their pay plans.”

–Dayna Harris, Partner, Farient Advisors

Compensation Metric Usage by Sector

In examining these plans more closely, we found many of the companies combine E&S compensation metrics with other metrics into an overall category that is generally not weighted more that 10 percent of the overall short term incentive award. And, in addition to not being tied to a significant amount of compensation, the goals around these metrics aren’t generally well defined or aren’t disclosed at all.

Companies and Their Approaches to E&S

As mentioned above, E&S metrics are most often found in the energy sector. Scientists estimate emissions from just 90 companies contributed for nearly 50 percent of the rise in global mean surface temperature since the end of the Industrial Revolution, and rightly so, energy companies are in the crosshairs of investors as it relates to global warming.

Chevron is the biggest individual company contributor to this rise in global mean surface temperature. Although it links 15 percent of STI to “environmental impact,” this metric is associated with direct environmental impact for spills. On the activism front, three shareholder proposals on E&S topics failed to get majority support: a Report on Transition to a Low Carbon Business Model, Report on Methane Emissions, and Requirement that a Director be Nominated with Environmental Experience. However, Chevron is starting to take notice. In its latest climate report, the company said it aims to reduce methane and flaring intensity by up to 30 percent from 2016 levels by 2023, and a newly created Environmental, Social and Governance (ESG) team will regularly engage with investors and other key stakeholders to understand and respond to ESG reporting preferences. It remains to be seen how Chevron ties these goals to executive pay.

Compare Chevron’s response to that of Royal Dutch Shell, which has also created specific goals to reduce its net carbon footprint – by about half by 2050, with an interim step of a 20 percent reduction by 2035. In addition, although not yet disclosed, the company has pledged to link these targets to its executives’ compensation. It will be interesting how they create this connection, particularly given the long timeframe of the goals.

Diversity is also top of mind with shareholders. Textron has taken the step of creating specific diversity goals and tying them to a portion of CEO compensation. Five percent of the CEO’s annual bonus is tied to “Improvement in Workforce Diversity” defined as the change in the number of U.S. full-time salaried diverse employees in relation to all full-time U.S. salaried employees. Verizon has a similar metric in its plan, tying five percent of annual bonus to having at least 58.9 percent of U.S.-based workforce comprise minority and female employees, and directing at least $4.6 billion of its overall supplier spending to minority- and female-owned firms.

Rally Points

The integration of specific E&S goals into compensation plans seems to lag that of shareholder focus. The pressure on companies to fully disclose their environmental and social positions should only increase with investors demanding specific goals tied to “real” compensation outcomes.

With an eye toward the future of specific E&S financial metrics, Farient suggests compensation committees consider the following:

- Be specific in E&S definitions and objectives, and link them to “real” compensation outcomes

- Deconstruct decades-long goals into shorter milestones and link integrate interim steps in to the current three-year performance period structure

- Dare to be different and consider long-term strategic goals in compensation plans that may also have a discretionary component

** Thank you to Main Data Group, which provided data for this Farient Brief.

© 2026 Farient Advisors LLC. | Privacy Policy | Site by: Treacle Media