Farient Advisors Point of View—Implications of the Proposed SEC Pay for Performance Disclosure Rules

May 6, 2015

On April 29, the SEC proposed rules, in accordance with Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 that will require companies to disclose the relationship between compensation “actually” paid to executives and the financial performance of the company.

Rules at a Glance

The proposed rules will:

- Aim to provide greater transparency and better inform shareholders when voting on the election of directors and executive compensation plans

- Require a new table in the proxy, showing up to 5 individual years’ total compensation as reported in the summary compensation table vs. “actual” pay, as well as a company’s TSR vs. that of its peer group

- Require the explanation of the data provided in either a narrative and/or graphic format

The proposed rule mandates that a table disclosing the relationship between “actual” pay and company performance (as indicated by TSR) be included in the proxy. More specifically:

- The table will show compensation data for the CEO and the average all other NEOs

- The amount “actually” paid will adjust the Summary Compensation Table (SCT) amount to include only the pension value applicable to that year of service, and the equity value based on fair value at vesting vs. grant date

- The table will require 3 years of disclosure in the first year, 4 years in the second year, and 5 years in the third year and thereafter

Actual Compensation, Simply Put

“Actual” compensation, as defined by the SEC, should essentially be looked at as “vested” compensation. In accordance with the rules, “actually” paid equals:

| The SCT total compensation | |

| Minus: | The change in pension value |

| Minus: | The grant date equity value |

| Plus: | The pension value applicable to that year of service |

| Plus: | The fair value as of vesting date for equity |

- Pension Value added back should be the actuarially determined service cost for services rendered in the applicable year (excludes changes in interest rates, executive’s age, and other actuarial inputs regarding previous accrued benefits) as defined in FASB ASC Topic 715

- Equity Value added back is the fair value as of the vesting date for equity vesting in that year consistent with fair value measurement guidance in FASB ASC Topic 718. This means, for example, that options will be valued at their fair market in-the-money or out-of-the money value in accordance with an option pricing model at the date of vesting

An Example

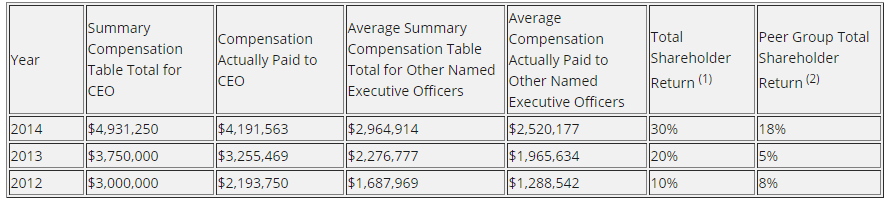

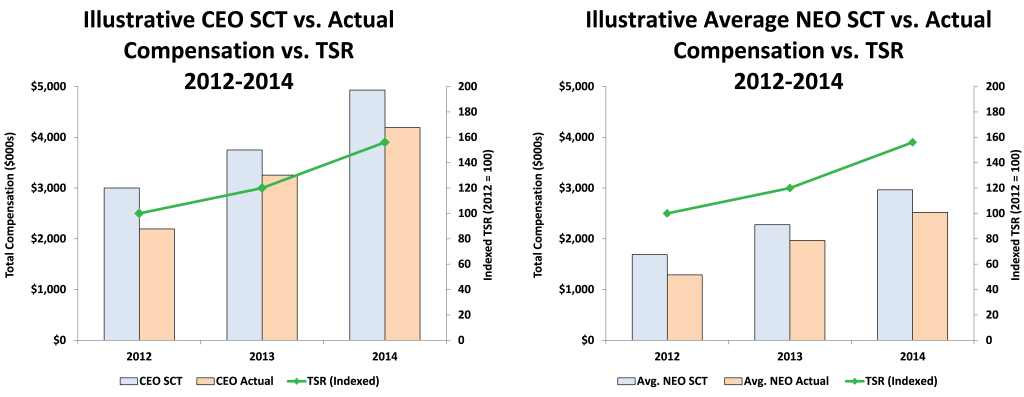

An illustration of what the new proposed table and the accompanying graphic might look like is shown below: (shown for the CEO only for illustrative purposes)

Illustrative Pay for Performance Table (2012 – 2014)

Farient Perspectives

While there are always pluses and minuses to any proposal, we feel as though, on balance, the SEC’s proposed rules are reasonable. The positive aspects of these rules are:

- It will force companies to explain and demonstrate the link between pay and performance. In the eyes investors, this is a good thing, as long as the explanation is concise and doesn’t just open the door to a more long-winded proxy

- Five years of data ultimately will need to be disclosed. In determining the link between pay and performance, it is often difficult to demonstrate a link one year at a time. This is because long-term incentive values can be lumpy, and each year may involve special circumstances. Looking at pay vs. performance over the longer term will help explain anomalies

- The measures of performance are TSR and relative TSR. These are the measures that investors rely on for determining their performance. Companies can always discuss additional measures if they feel as though TSR and relative TSR do not tell the full story

- Options are valued at their fair market value, rather than intrinsic value, which puts them on equal footing with other equity vehicles. This means that companies are not advantaged or disadvantaged by which long-term incentive vehicles they offer

- Further, options and other equity vehicles are valued upon vesting, not exercise. This removes executive discretion from when those grants will be valued

- Total compensation is considered, which means that companies won’t be advantaged or disadvantaged based on pay mix

- Pensions are valued without regards to uncontrollable events, like interest rates and mortality rates

- Using a standardized calculation method will allow investors to compare pay for performance relationships across companies

- The rules allow for a phase-in of 3 reporting years, moving to 5 years

On the negative side, a significant issue with the proposed rules is that the time horizon of the pay measured will not necessarily match the time horizon of the performance measured. In other words, awards vested for a given performance plan cycle may not correspond to years for which the TSR is shown in the table. In addition, those companies using measures that drive shareholder value (rather than using shareholder value, like TSR or relative TSR, directly), may experience a lower correlation of awards to value in any given period compared to those using shareholder value directly. These and any other issues with the prescribed disclosures may warrant additional explanations and/or disclosures at the discretion of the issuer.

Action Items

Now that we’ve heard from the SEC, companies have the opportunity to take the following steps:

- Calculate “actual” pay in accordance with the proposed rules

- Mock-up the required table, as well as the narrative and graphical disclosures

- Determine whether any supplemental data, in addition to the data required by the SEC, should be discussed in the Compensation Discussion &Analysis (CD&A)

- Determine how this disclosure likely will fit into the CD&A, and how explanations can be kept succinct

- Determine how the narrative can be used to improve transparency and investors’ understanding of the company’s executive pay programs. Determine whether this disclosure is likely to affect investors’ views of the pay programs, and ultimately the company’s Say On Pay vote. If the impact is negative, determine whether and how best to modify program design

- Provide any comments to the SEC on the proposed rules by the end of the comment period on June 30, 2015

© 2026 Farient Advisors LLC. | Privacy Policy | Site by: Treacle Media