Putting The Long-Term Back Into Long-Term Incentives

June 28, 2016

There has always been tension between making long-term incentives both motivational and competitive, while at the same time aligning pay design with the longer-term interests of shareholders. Thus is the case with performance and vesting periods. Shorter periods are considered to be good for the talent (motivational and competitive), while longer periods are considered to be good for investors (alignment). The equilibrium for performance and vesting periods has seemed to settle on an average of three years – just short enough to provide line of sight and a reasonable time frame for goal-setting, and just long enough to demonstrate a track record for sustainable shareholder returns.

Having said this, the SEC, investors, and proxy advisors all have tried to put more teeth into long-term sustainable performance through such mechanisms as claw backs and ownership guidelines. Another solution to “having your cake and eating it too” (i.e., having a competitive vesting period while also tying executives to longer-term sustained performance) is to institute post-vesting holding requirements. In a nutshell, post-vesting holding requirements separate the vesting event from the liquidity event so the executive has to hold onto all (or a portion) of his or her net after-tax shares, even after vesting, for a given period of time. This helps to keep the risk of forfeiture in check because the shares are vested, and therefore portable in the case of termination, but remain subject to share price performance during the holding period.

Holding periods are becoming more and more intriguing to compensation committees and corporate governance experts for three primary reasons:

• First, financial performance tends to be correlated with shareholder value over longer, sustained periods of time (e.g., five years of financial performance tends to correlate more closely to market performance than three years or one year of financial performance). As a result, holding requirements help improve the alignment between executive and shareholder interests, as well as between performance and executives’ realizable pay

• Second, with the pending implementation of clawback policies by the SEC, compensation committees are wondering how they are going to recoup shares that must be clawed back, particularly from executives who have left the company. Holding requirements help solve the recoupment issue

• Third, companies get additional points in ISS’ Equity Plan Scorecard for requiring holding periods, thus potentially earning them support for a higher number of authorized shares

Because of these reasons, holding requirements are now considered to be yet another indicator of good governance among investors and proxy advisors.

Trends In Holding Requirements

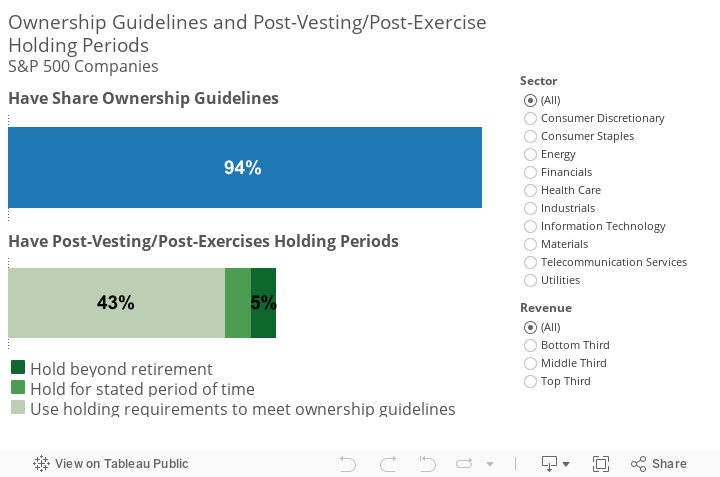

Most post-vesting holding requirements are simple – they require executives to hold a certain percentage of net after-tax shares earned in their equity incentive plans until their stock ownership guidelines are met. As shown in the chart below, approximately half of S&P 500 companies have post-vesting/post-exercise holding requirements, most of which are designed to ensure that share ownership guidelines are met. For these companies, the termination of an executive makes ownership guidelines, and the associated holding requirements, moot. As a result, shares are not necessarily available from these executives for clawbacks.

Accordingly, there is a small, but emerging cadre of companies (10%) that apply holding requirements to all shares, regardless of whether or not ownership guidelines are met because these types of holding requirements address the clawback issue.

Post-Vesting/Post-Exercise Holding Periods, S&P 500 Companies

Designing for Intended Outcomes Vs. Unintended Consequences

While holding periods sound like the perfect antidote to short-termism, they may carry unintended consequences. For example, the requirement to hold until/beyond retirement may encourage early retirement if the executive desires liquidity or portfolio diversification. There also are concerns that executives who are highly leveraged to their company’s stock may cause them to be unduly risk averse. Second, if there is a post-exercise holding period on the company’s options, then executives may be encouraged to exercise earlier rather than later following vesting, causing them to be less leveraged to the stock.

The good news is that these unintended consequences can be avoided by making thoughtful design choices. One of the most important trade-offs is to manage the percentage of net shares to be held vs. the time horizon of the requirement. In general, the higher the percentage of net shares to be held, the shorter the holding period typically is. This is why companies with stated holding periods typically require 100% of the net shares to be held for one year. Conversely, companies that require holding through retirement typically require 25 to 50% of the net shares to be held. In the case of stock options, narrowing the window between vesting and term may address the issue of early exercise.

In thinking about feature design, we also should remember that the required lookback period for clawbacks will be three years. As a result, holding periods may extend beyond the typical one-year periods of today to something closer to three years.

The Future Of Holding Requirements

I expect the number of companies requiring post-vesting/post-exercise holding to continue to grow. Today, most of these requirements apply to executives who are building toward ownership guidelines, but the emerging trend is to apply holding requirements to all shares, particularly for the highest level executives. Putting the “long-term” back into long-term incentives will help drive alignment between executives and shareholders, hopefully creating a win/win for executives and shareholders alike.

Read on Forbes© 2026 Farient Advisors LLC. | Privacy Policy | Site by: Treacle Media